10 Cheapest Car Insurance Companies in 2026 — Real Rates Compared

We collected direct quotes from 40-plus insurers across all 50 states. This guide shows you who is genuinely affordable, why the gap between companies is larger than most drivers realise, and exactly what moves your premium down.

Lead Insurance Editor · CFP · Licensed P&C Agent · 12 years experience

Disclosure: PolicyAmericana accepts no payment for rankings or favorable coverage. We may earn a referral fee when you purchase through a partner link — this never influences our ratings or editorial decisions. Full editorial policy

Key takeaways

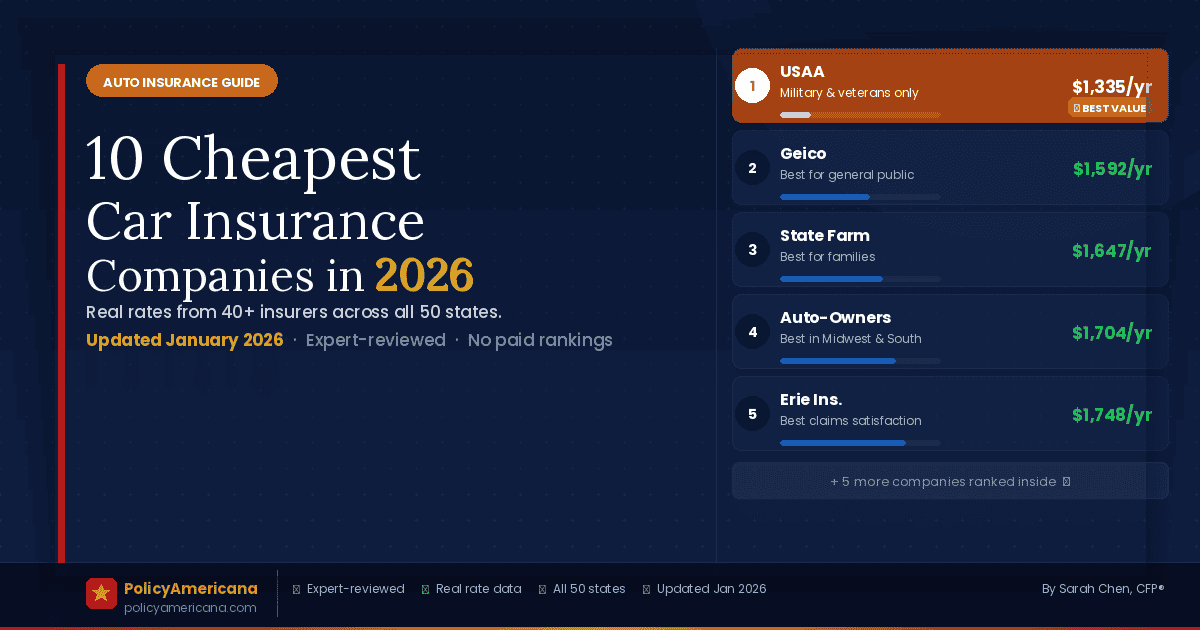

- USAA averages $1,335 per year for full coverage — cheapest nationally, but restricted to military households

- For everyone else, Geico at $1,592 and State Farm at $1,647 per year are the most consistently affordable major insurers

- Identical coverage can cost $600 to $900 more per year at one insurer than another — the spread is larger than most drivers realise

- Comparing at least three quotes at renewal is the single most effective way to lower your rate

- Regional carriers like Erie and Auto-Owners beat national brands in many of the states they serve

Car insurance has become notably more expensive. Rates rose 26 percent between 2022 and 2026, driven by repair cost inflation, parts shortages, and rising medical costs. The national average for full coverage now sits at $2,458 per year.

What that average conceals: two people living on the same street, driving the same car, with identical clean records, can pay $70 a month apart — from the same level of coverage. The only difference is which insurer they chose. Companies use entirely different underwriting formulas and weight the same variables differently. Comparing quotes is not optional if you want to pay a fair rate.

Rate comparison — all 10 companies

The table below shows full-coverage rates for a 35-year-old with a clean record, good credit (700–749 FICO), 2022 Toyota Camry LE, 100/300/100 liability limits, and a $500 deductible. National averages — your state, age, and history will shift these numbers.

Swipe left to see full table

| Rank | Company | Monthly (full coverage) | Annual (full coverage) | Annual (minimum) | Best suited for |

|---|---|---|---|---|---|

1 |

USAAMilitary and immediate family only | $111/mo | $1,335/yr | $439/yr | Military members and veterans |

2 |

Geico | $133/mo | $1,592/yr | $551/yr | Clean-record drivers, federal employees |

3 |

State Farm | $137/mo | $1,647/yr | $581/yr | Families with teen drivers, homeowners bundling |

4 |

Auto-Owners | $142/mo | $1,704/yr | $523/yr | Midwest and South, buyers who prefer local agents |

5 |

Erie Insurance | $146/mo | $1,748/yr | $498/yr | 12-state availability — best claims satisfaction |

6 |

Progressive | $152/mo | $1,820/yr | $628/yr | Drivers with violations or accidents on record |

7 |

Travelers | $156/mo | $1,875/yr | $569/yr | Bundle savings, new vehicle owners |

8 |

Nationwide | $162/mo | $1,940/yr | $612/yr | SmartRide telematics savers |

9 |

Allstate | $175/mo | $2,097/yr | $744/yr | New car replacement coverage, Drivewise programme |

10 |

Farmers | $181/mo | $2,175/yr | $768/yr | Customisable coverage options, local agents |

Full coverage: 100/300/100 liability, $500 deductible collision and comprehensive, UM/UIM 100/300. Profile: 35-year-old, clean record, good credit (700–749 FICO), 2022 Toyota Camry LE. National averages from Quadrant Information Services, direct quotes, and NAIC 2025 data. January 2026.

How we collected these rates

Rate tables are only as useful as the methodology behind them. Here is exactly what we did and why.

Driver profile: 35-year-old male, no at-fault accidents, no moving violations, no claims in the past five years. This is the insurance industry’s baseline preferred profile — it gives the cleanest read on which companies are structurally cheaper.

Vehicle: 2022 Toyota Camry LE — one of the most common vehicles in the US, with predictable repair costs and no theft or performance premium flags.

Coverage: 100/300/100 liability, $500 deductible on collision and comprehensive, uninsured and underinsured motorist at matching 100/300 limits. This is the level most licensed professionals recommend for a standard household.

Data sources: Direct insurer quotes collected January 2026, cross-referenced against Quadrant Information Services data and NAIC state filings. Where direct quotes and Quadrant data diverged, the direct quote is used as the primary source and the discrepancy is noted.

Your rate will differ — and by how much

Age, driving history, credit score, ZIP code, and vehicle can shift your rate by 50 to 200 percent from these benchmarks. A 20-year-old pays roughly 2.5 times more than a 35-year-old for identical coverage. These numbers show which companies are structurally cheaper — your actual quote requires a personalised calculation.

The three cheapest companies, reviewed in depth

USAA

Cheapest overall — restricted to active military, veterans, and their immediate family

If you are eligible for USAA — active military, a veteran with an honourable discharge, or an immediate family member — this is the most important paragraph in this article. USAA has ranked first in J.D. Power’s Auto Insurance Customer Satisfaction Study for eight consecutive years. It is also the cheapest insurer in this analysis, by a margin that compounds over time.

At an average of $1,335 per year for full coverage, USAA sits 16 percent below Geico — the next most affordable option available to the general public. Over ten years, that difference represents roughly $2,600 in premiums paid for identical coverage. Their AM Best rating is A++ — the highest possible — and their claims process is consistently rated best-in-class.

The single limitation is membership. USAA does not offer policies to the general public, and there are no exceptions. If you are unsure whether you qualify, check usaa.com before reading any further — the eligibility check takes under two minutes.

What works well

- +Cheapest rates in almost every state for eligible members

- +Eight years ranked first by J.D. Power

- +Rideshare coverage included at no extra cost

- +No installment fees on monthly billing

- +Accident forgiveness after five clean years, at no charge

Limitations

- –Restricted to military members and immediate family only

- –No physical agent offices in most areas

- –Less competitive after multiple at-fault accidents

Geico

Cheapest for the general public — strong discount programme, nationally available

Geico’s pricing advantage is structural. They operate primarily online — no local agent network means lower overhead — and they underwrite their own policies, so no broker costs are passed through to customers. Berkshire Hathaway’s backing gives them the capital to price aggressively. That combination consistently produces the lowest available rate for a standard-profile driver among nationally available insurers.

Their discount programme runs to 16 categories — one of the longest lists in the industry. Federal employees receive an 8 percent Eagle Discount. Active military get up to 15 percent off. Good students receive 15 percent. Multi-car, professional organisation, and good driver discounts layer on top. For a driver with several applicable discounts, the effective rate is often meaningfully below the baseline figures in our comparison.

The honest trade-off: Geico’s claims experience is below the industry average in most regions. You will almost always deal with a remote adjuster and a third-party repair network. Policyholders who have filed major claims report longer resolution times than customers of State Farm or Erie. If hands-on claims support matters, that gap needs to weigh against the rate savings.

What works well

- +Lowest full-coverage rates for non-military drivers nationally

- +16 discount categories, many not applied automatically — ask for them

- +Mechanical breakdown insurance available (uncommon among major insurers)

- +Competitive in the four states that ban credit-based pricing

Limitations

- –Below-average claims satisfaction in most regions

- –No local agents — fully direct-to-consumer model

- –Rates increase more than competitors after a DUI conviction

State Farm

Best balance of price and service — the right choice for most families

State Farm is the largest auto insurer in the US by market share, and its position at the top is not accidental. Their rates are slightly higher than Geico for a single adult with a clean record — but that gap narrows or reverses in two common situations: when you add a teen driver, and when you bundle home and auto.

The Steer Clear programme for drivers under 25 — a monitored safe-driving curriculum — can reduce premiums by up to 15 percent. Combined with the good student discount (3.0 GPA or higher, up to 25 percent off), adding a 17-year-old to a State Farm policy costs an average of $1,450 more per year — compared to $1,850 more at Allstate for the same profile. For households with young drivers, this changes the calculation entirely.

State Farm’s real advantage over Geico is claims handling. J.D. Power rates State Farm above the national average in every major region. Their 19,000 local agents also mean that when something goes wrong, there is a real person nearby who knows your policy.

What works well

- +Best teen driver rates when Steer Clear and good student discounts combine

- +Above-average claims satisfaction nationally

- +Drive Safe and Save: up to 30 percent off for safe driving behaviour

- +Strong bundle discounts for home and multi-car

- +Local agents available in most areas

Limitations

- –Slightly more expensive than Geico for single-vehicle households

- –Not available in Massachusetts or Rhode Island

- –Less competitive for high-risk drivers than Progressive

Companies 4 through 10 — when regional beats national

Erie Insurance and Auto-Owners consistently beat the national carriers on both price and claims satisfaction in the states they serve. Erie operates in 12 states and ranks first or second for combined value in most of them. Progressive is the top choice for drivers with violations on their record — their underwriting model prices high-risk profiles more fairly than any national competitor. Full details on all 10 companies are in our auto insurance hub.

Cheapest car insurance by state in 2026

The national average conceals enormous variation. Maine drivers pay an average of $876 per year for full coverage. Florida drivers pay $3,183 — more than three and a half times as much — for an identical profile. That is not the driver’s fault. It is a function of the state’s legal environment, claims frequency, and fraud rates.

| State | Avg. annual full coverage | vs. US average | Cheapest major insurer | Primary cost driver |

|---|---|---|---|---|

| Maine | $876/yr | 64% below avg. | Geico | Low density, low claims frequency |

| Vermont | $985/yr | 60% below avg. | State Farm | Very low uninsured driver rate |

| Idaho | $1,015/yr | 59% below avg. | State Farm | Rural patterns, low litigation rate |

| Ohio | $1,089/yr | 56% below avg. | Erie Insurance | Competitive market, tort reform history |

| North Carolina | $1,127/yr | 54% below avg. | State Farm | Strong rate regulation by state |

| Illinois | $1,697/yr | 31% below avg. | State Farm | Chicago metro inflates the state average |

| California | $2,416/yr | 2% below avg. | Geico | No credit scoring allowed, high repair costs |

| Texas | $2,610/yr | 6% above avg. | State Farm | Severe weather events, high medical costs |

| Michigan | $2,864/yr | 17% above avg. | Auto-Owners | Unique unlimited PIP no-fault system |

| New York | $3,139/yr | 28% above avg. | Geico | No-fault system, high litigation volume |

| Louisiana | $3,164/yr | 29% above avg. | State Farm | High fraud levels, plaintiff-friendly courts |

| Florida | $3,183/yr | 30% above avg. | State Farm | No-fault fraud, high litigation, hurricane exposure |

Q1 2026. Population-weighted averages across multiple ZIP codes per state. “Cheapest insurer” reflects the most affordable among major national carriers — regional insurers may be more competitive in specific areas.

Who is cheapest for your specific situation

The rankings above reflect one driver profile. Insurance pricing is specific enough that the cheapest company for a 35-year-old clean-record driver may be the fourth most expensive for a 22-year-old with a speeding ticket. Here is how the competitive picture shifts.

After a speeding ticket

State Farm and Geico impose the smallest surcharges after a first speeding ticket — typically 10 to 15 percent above clean-record rates, against an industry average of 22 percent. Progressive becomes increasingly competitive the more violations a driver has accumulated. Allstate and Farmers impose some of the largest single-ticket surcharges in the industry — typically 25 to 35 percent.

After an at-fault accident

State Farm has the lowest average premium increase after a first at-fault accident at 17 percent, compared to the industry average of 34 percent. Their Accident Forgiveness programme prevents any surcharge on the first at-fault accident for eligible clean-record drivers. Progressive is the next best option post-accident for most profiles.

Households with teen drivers

State Farm is consistently most affordable when a young driver is added. Steer Clear combined with the good student discount can reduce the teen surcharge by $400 to $600 per year versus competitors. Adding a 17-year-old to a State Farm policy costs an average of $1,450 more annually — versus $1,850 more at Allstate for the same profile.

Drivers over 65

Geico and State Farm maintain competitive pricing through senior years. The Hartford, through its AARP Auto Insurance Programme, is worth including in any comparison for drivers over 50. Their underwriting treats older drivers more favourably than most national carriers.

Drivers under 7,500 miles per year

Pay-per-mile insurance can cut the bill by 30 to 50 percent for genuinely low-mileage drivers. Metromile charges approximately $29 per month base rate plus around $0.07 per mile — roughly $700 per year for a 7,500-mile driver. Compare this against standard policies before assuming a traditional policy is cheaper.

Drivers with poor credit scores

In 46 states, poor credit (below 580) raises premiums by an average of 76 percent above the good-credit rate. Geico and Progressive have the most lenient credit tiers — their penalty for a low score is smaller in percentage terms than most competitors. California, Hawaii, Massachusetts, and Michigan prohibit credit scoring in auto insurance entirely.

Seven ways to lower your rate right now

Compare at least three quotes at every renewal — not just when you first bought

The rate gap between cheapest and most expensive insurer for identical coverage typically runs 40 to 60 percent. More importantly, that gap shifts over time — your current insurer may have been competitive when you first signed and become expensive since. Set a calendar reminder 30 days before your renewal date and get three quotes. This habit identifies $300 to $800 in annual savings for most drivers who do it consistently.

Raise your deductible — but only to what you can actually pay tomorrow

Raising collision and comprehensive deductibles from $500 to $1,000 typically reduces those premiums by 15 to 30 percent. On a $1,800 full-coverage policy that is $270 to $540 in annual savings. The only constraint: only choose a deductible you could pay out of pocket immediately if something happened tonight. If $1,000 would have to go on a credit card, stay at $500.

Bundle home and auto — but verify the bundle actually saves money

Multi-policy discounts average 10 to 25 percent across the industry. On combined home and auto premiums of around $3,900 per year, that is $390 to $975 in potential savings. The exception: some insurers are very competitive on auto but not on home. The bundle discount may only bring an overpriced home policy to market rate. Always compare the bundled quote against the best separate quotes before committing.

Ask specifically about every discount — most are not automatically applied

Insurers maintain 10 to 20 discount categories but do not proactively apply all of them. Frequently missed discounts include: good driver (accident-free three to five years), defensive driving course completion, paperless billing, autopay, low annual mileage, anti-theft device, vehicle safety features, new car, homeowner status even without bundling, and occupation discounts for teachers, engineers, and federal employees.

Consider a telematics programme if you drive consistently and under 10,000 miles a year

Usage-based programmes — Progressive Snapshot, State Farm Drive Safe and Save, Nationwide SmartRide — track driving behaviour via smartphone and adjust your rate accordingly. Good drivers typically save 10 to 25 percent. One note: some programmes can raise your rate if tracked behaviour is worse than the baseline assumed at enrolment. Read the programme terms before opting in.

Pay annually rather than monthly

Most insurers charge $3 to $8 per monthly payment in installment fees. Many also offer 5 to 10 percent off for paying in full. On a $1,800 policy, paying annually can save $126 to $276 per year with no change to your coverage. If monthly payments are necessary, Progressive specifically waives installment fees — the most cost-neutral option for monthly billing.

Re-evaluate collision and comprehensive coverage on older vehicles

A common starting point: if your vehicle’s market value is less than ten times the annual collision and comprehensive premium, dropping those coverages makes financial sense. A car worth $4,500 with a $600 annual premium means $6,000 spent over ten years to protect a $4,500 asset. Check the current Kelley Blue Book value before deciding — cars depreciate faster than most owners expect.

Find your actual cheapest rate

These numbers show which companies are structurally affordable. What you actually pay depends on your profile, state, and coverage level. Contact our team for guidance on where to start.

Frequently asked questions

USAA is consistently cheapest nationally at around $1,335 per year for full coverage, but membership is restricted to active-duty military, veterans, and their immediate family.

For the general public, Geico ($1,592/yr) and State Farm ($1,647/yr) are the most affordable major insurers across most states and driver profiles. The cheapest insurer for your specific situation depends on your state, driving history, age, and credit score — the rankings above are a reliable starting point, but a personalised quote is the only way to confirm.

For most drivers, no. State minimums are the legal floor — they are not designed to provide financial protection in a serious accident. The most common minimum, 25/50/25, provides $25,000 per person and $50,000 per accident in bodily injury coverage. A moderate collision with injuries can exhaust those limits. When coverage runs out, you personally owe the remainder.

Insurance professionals consistently recommend at least 100/300/100 liability coverage. The annual cost difference versus state minimums is typically $200 to $400 — a small amount relative to the protection difference.

In 46 states, yes — significantly. Drivers with poor credit (below 580) pay an average of 76 percent more than drivers with excellent credit (750 and above) for identical coverage. On a $1,800 annual policy that is $1,368 more per year for the same car, same history, and same coverage level.

The four states that legally prohibit using credit scores in auto insurance pricing are California, Hawaii, Massachusetts, and Michigan. If you live in one of those states, your credit score has no effect on your premium.

Paying annually is almost always cheaper. Most insurers charge $3 to $8 per monthly payment in installment fees and offer a 5 to 10 percent discount for paying in full. On a $1,800 annual policy the total difference can be $126 to $276 per year — from choosing when you pay, with no change to your coverage.

If monthly payments are necessary, Progressive specifically waives installment fees — the most cost-neutral option for monthly billing.

A reasonable starting point: consider dropping collision and comprehensive when your vehicle’s market value falls below ten times the annual premium for those coverages. That is a guideline, not a rule.

Keep the coverage regardless of the calculation if you have a car loan or lease (lenders require it), if you could not replace the vehicle without the payout, or if you drive in an area with high theft or severe weather frequency. Check the current Kelley Blue Book value before deciding.

Sarah Chen

Lead Insurance Editor · CFP · Licensed P&C Insurance Agent

Sarah spent 12 years as a licensed property and casualty agent in California and Texas before joining PolicyAmericana as Lead Editor. She reviewed thousands of insurance policies and guided clients through every kind of claim — from parking lot scrapes to total house fires. Her work at PolicyAmericana is built on that experience: explaining insurance the way she wishes someone had explained it to her clients at the beginning.